Usual Answers To Home Mortgage Questions

Content create by-Omar HooperWhat can I do to get a great mortgage? How can I find low rates I can afford? What should I know before I talk to any lenders? When do I start the process? How can I find answers to all of these questions and more? Read on for expert mortgage advice.

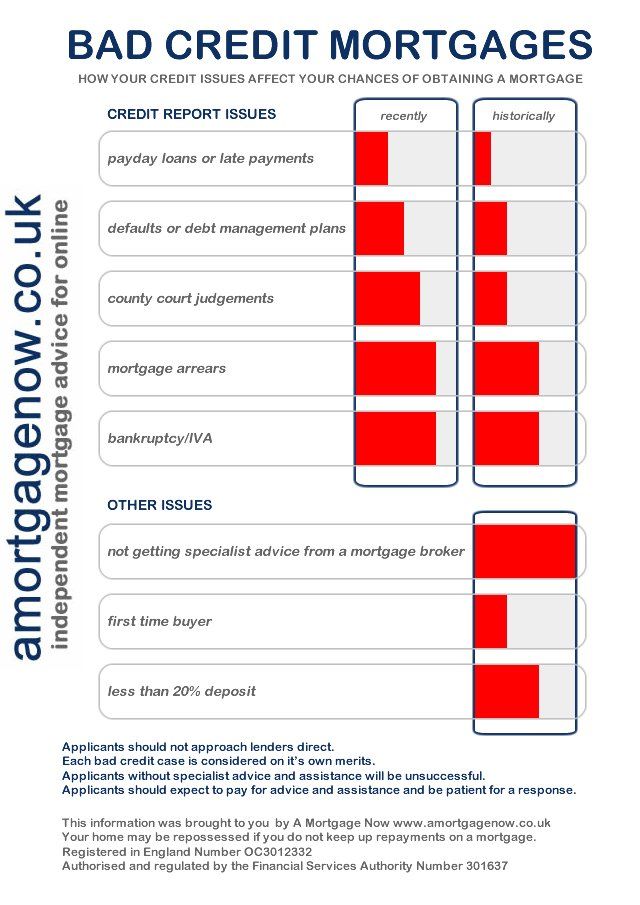

Before trying to get a mortgage approval, find out your credit score. Mortgage lenders can deny a loan when the borrower has a low credit score caused by late payments and other negative credit history. If your credit score is too low to qualify for a mortgage loan, clean up your credit, fix any inaccuracies and make all your payments on time.

Start preparing for getting a home mortgage early. Get your financial business in order. You have to assemble a savings stockpile and wrangle control over your debt. Delays can cause you to lose your chance at mortgage approval.

Getting the right mortgage for your needs is not just a matter of comparing mortgage interest rates. When looking at offers from different lending institutions you must also consider fees, points and closing costs. Compare all of these factors from at least three different lenders before you decide which mortgage is best for you.

Start saving all of your paperwork that may be required by the lender. These documents include pay stubs, bank statements, W-2 forms and your income tax returns. Keep these documents together and ready to send at all times. If you don't have your paperwork in order, your mortgage may be delayed.

You may be able to add your homeowners insurance costs to your mortgage payment. One advantage of this is negating the need to make two payments. Instead of paying your mortgage and an insurance bill, you can pay both bills in one payment. If you like to consolidate your bills, this is a good idea.

You might want to hire a consultant to assist you with the mortgage process. There are lots of things involved with the process and a consultant will be able to get you a great deal. You'll also be sure that the all is on the up and up when you've got the knowledge of a consultant at your fingertips.

When rates are near the the bottom, you should consider buying a home. If you do not think that you will qualify for a mortgage, you should at least try. Having your own home is one of the best investments that you can make. Quit throwing away money into rent and try to get a mortgage and own your own home.

When financing a house, giving a large down payment will result in a lower mortgage rate. This is due to the fact that a big down payment will reduce your loan to value ratio. When the loan to value ratio gets lower, the interest rates become more favorable for the home buyer.

Save up for the costs of closing. Though you should already be saving for your down payment, you should also save to pay the closing costs. They are the costs associated with the paperwork transactions, and the actual transfer of the home to you. If you do not save, you may find yourself faced with thousands of dollars due.

When trying to figure out how much of a mortgage payment you can afford every month, do not neglect to factor in all the other costs of owning a home. There will be homeowner's insurance to consider, as well as neighborhood association fees. If you have previously rented, you might also be new to covering landscaping and yard care, as well as maintenance costs.

Be careful when taking out a second line of financing. Many financial institutions will allow you to borrow money on your home equity to pay off other debts. Remember you are not actually paying off those debts, but transferring them to your house. Check to make sure your new home loan is not at a higher interest rate than the original debts.

Before you even start looking at a new home to buy, try to get pre-approved for a home. This will give you confidence when looking for a new home and let you know what your budget is. It will also save you from choosing a home only to find out you cannot secure a large enough loan to purchase it.

Ask around about mortgage financing. You may be surprised at the leads you can generate by simply talking to people. Ask your co-workers, friends, and family about their mortgage companies and experiences. They will often lead you to resources that you would not have been able to find on your own.

If you have previously been a renter where maintenance was included in the rent, remember to include it in your budget calculations as a homeowner. A good rule of thumb is to dedicate one, two or even three perecent of the home's market value annually towards maintenance. This should be enough to keep the home up over time.

Know the real estate agency or home builder you are dealing with. It is common for builders and agencies to have their own in-house financiers. Ask the about their lenders. Find out see here now . https://www.pa.gov/guides/get-vaccinated/ could open a new avenue of financing up for your new home mortgage.

Be sure that you know exactly how long your home mortgage contract will require you to wait before it allows you to refinance. Some contracts will let you within on year, while others may not allow it before five years pass. What you can tolerate depends on many factors, so be sure to keep this tip in mind.

If you have less than perfect credit, one way to overcome it is to have a large down payment, more than most other borrowers. It is common for people to save between three and five percent, but you should aim for around twenty if you want to increase your chances of being approved.

As was stated in the introductory paragraph of this article, the mortgage financing process is very complicated. It can seem indecipherable to a real estate novice. The key to financing a great mortgage that allows you to buy the home of your dreams is to educate yourself on the mortgage process. Study the mortgage tips and advice in this article very carefully.